.png)

Key Takeaways

- tBTC supply held; DeFi deployment increased in BTC terms: tBTC supply ended Q1 at 5.9k, unchanged QoQ (-0.03%) and +32% YoY, while DeFi TVL (BTC) rose +19% QoQ to 7k BTC, led by Aave supplied tBTC reaching ~2.1k (+24% QoQ).

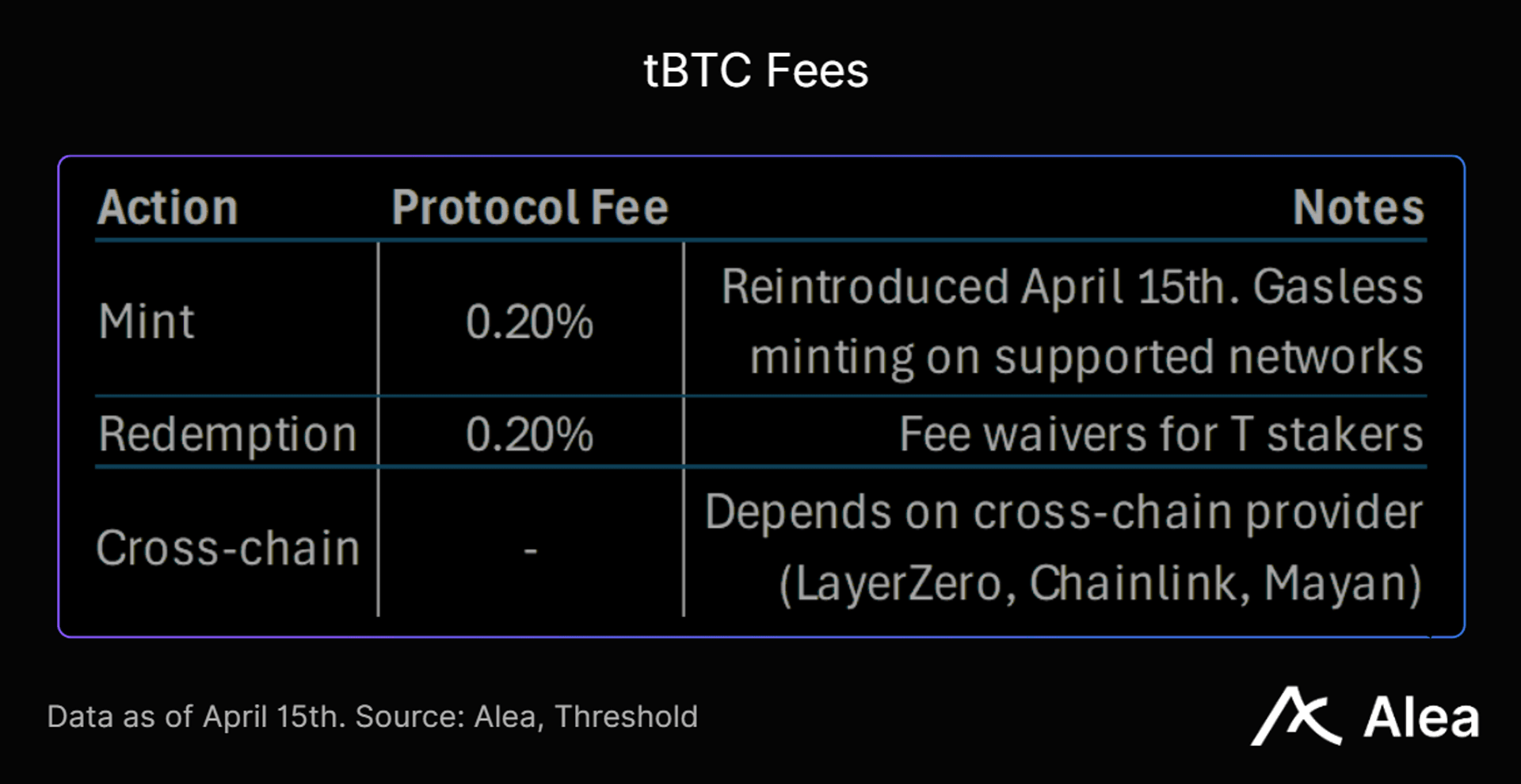

- Annualized fees declined -51% QoQ to $712k: Q1 fee capture came only from redemptions and was further reduced by the Jan. 22 redemption fee waiver for eligible T stakers. The Apr. 15 mint-fee activation broadens monetization from exit-only to entry-and-exit flows (20bps mint fee + 20bps redemption fee).

- tBTC supply turnover is balanced: 2,099 tBTC minted and 2,101 burned, equal to 2.9x annualized total turnover. At 20 bps on both mint and redemption, the same turnover would imply ~34 BTC, or ~$2.3M, in annualized revenue at quarter-end BTC price, versus $712K in Q1.

- The token repriced lower while tBTC’s liquidity position improved: T fell -30% QoQ to ~$67M FDV / market cap, with ~100% float and no unlock overhang. TVL-linked valuation improved, with DeFi TVL/FDV rising +13% QoQ to 7.4x, but fee-linked valuation worsened as P/F rose to 95x.

Relevant data guidelines: The report’s data cut-off date is March 31st. Annualized = trailing 30-day run-rate (or specified in caption). Quarterly values are end-of-period unless explicitly labeled ‘average’ in the chart/table.

Updates on Mint and Redemption Fees

Threshold’s economics are flow-based. In Q1-26, protocol fees came only from the 20 bps redemption fee. The 20 bps mint fee was reactivated on Apr. 15, 2026, after quarter-end, expanding monetization from exit-only activity to both mint and redemption flows.

T is the governance and staking token. Stakers can receive tBTC redemption fee waivers, while protocol revenue funds the treasury and discretionary open-market T buybacks (it is not a fixed distribution policy).

Financial Report

Threshold exited Q1 with stronger BTC-denominated deployment than USD optics suggest, but weaker realized monetization. tBTC supply ended the quarter at 5.9k, flat QoQ and +32% YoY. DeFi TVL rose +19% QoQ in BTC terms to 7k BTC, led by Aave supplied tBTC reaching ~2.1k, up +24% QoQ. USD DeFi TVL fell -7% to $481M because BTC declined -22% QoQ.

Fees moved in the opposite direction. Trailing-30-day annualized fees fell -51% QoQ to $712K. BTC-denominated annualized revenue fell -38% QoQ to ~10 BTC, so the decline was not only price-driven. Q1 monetization remained redemption-only, and effective fee capture was reduced by the Jan. 22 redemption fee waiver for T stakers.

The key operating distinction is supply versus flow. tBTC supply can stay flat while fees fall if users hold and deploy tBTC instead of minting or redeeming. In Q1, trailing 90-day flows were balanced: 2,099 tBTC minted and 2,101 burned, equal to 2.9x annualized total turnover. That turnover becomes more valuable in Q2 after the Apr. 15 mint-fee activation.

At Q1’s 2.9x turnover, a 20 bps fee on both mint and redemption flows would imply ~34 BTC of annualized revenue, or ~$2.3M at quarter-end BTC price. Reversion to the historical 5.24x turnover average would imply ~$4.2M. Both scenarios assume no material flow elasticity and unchanged fee-waiver mix.

tBTC Performance Metrics

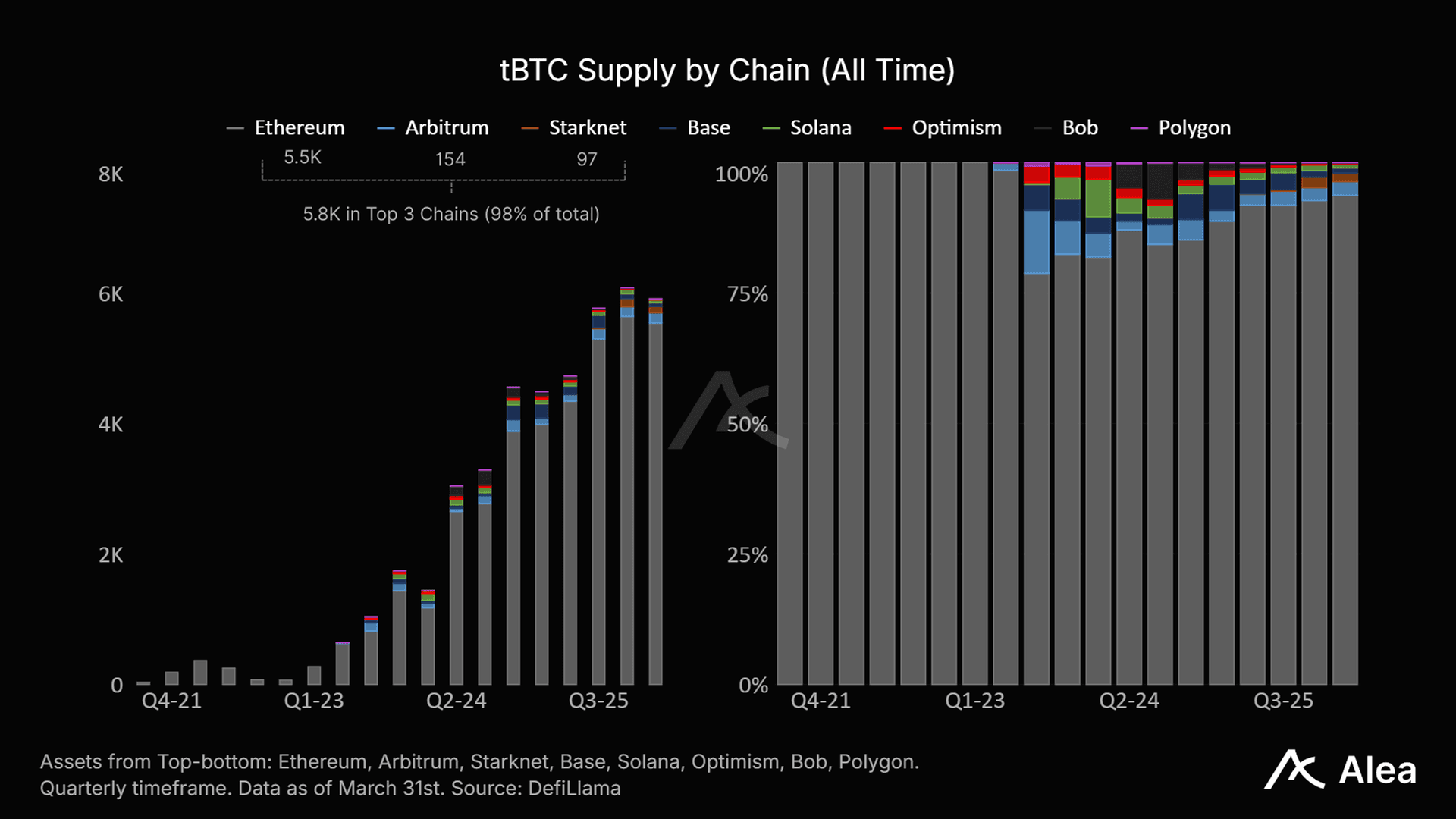

tBTC ended Q1-26 at 5.9k, flat QoQ and +32% YoY. Supply held through a -22% BTC drawdown, suggesting holders did not redeem back to native BTC in size despite BTC’s price decline.

tBTC’s chain expansion strategy began in H2 2023. As of Q1-26, supply remains concentrated on Ethereum L1 (94%), followed by Arbitrum (2.6%), Starknet (1.6%), and Base (~1%). The largest absolute gain YoY was Ethereum with +1.5k tBTC increase (+39%), followed by Arbitrum, with a +56 tBTC increase (+62%).

DEX activity weakened. Annualized tBTC DEX volume fell -67% QoQ in USD terms and -58% in BTC terms. Activity concentrated on Curve Ethereum, partly because YieldBasis volume is reported within Curve. This separates two Q1 realities: collateral deployment improved, while secondary-market turnover cooled.

tBTC is deployed across a range of protocols, with 26 of 55 (>$10k) holding >$1M of tBTC. Out of the top 25 addresses that hold tBTC across chains, 19 are identifiable protocols; the remaining six are unlabelled wallets.

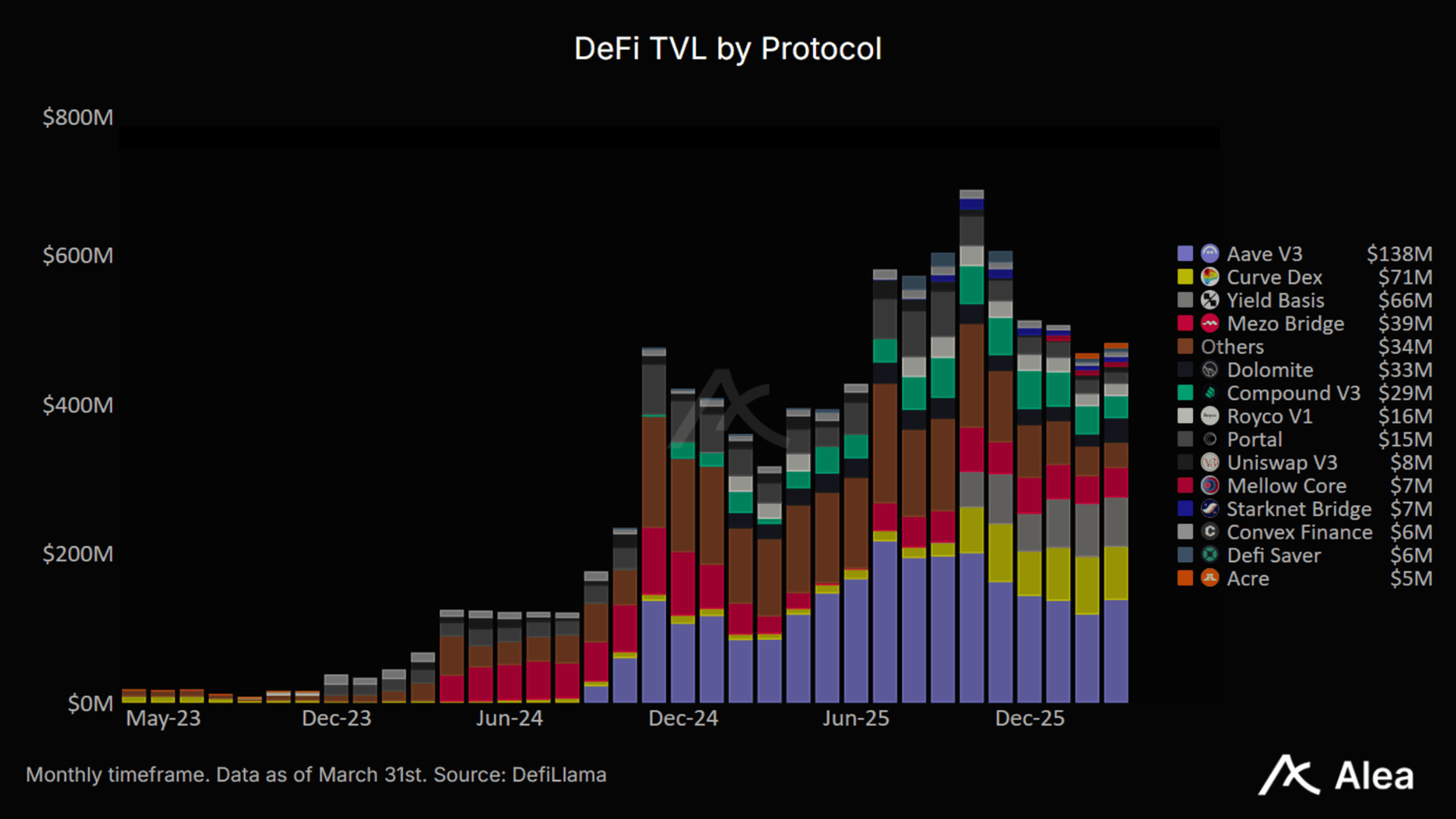

tBTC’s Aave growth in Q1 was the largest contributor to DeFi TVL increase, reaching ~2.1K tBTC supplied as collateral by the end of the quarter (+24% QoQ). Most tBTC is used as collateral rather than borrowed, keeping supply APR near its historical average of ~0.01%.

Growth is concentrated in a few high-utility venues. Aave V3 held $138M, or 29% of DeFi TVL, and was the largest contributor to BTC-denominated growth. Curve held $71M, while YieldBasis held $66M. Together, Aave, Curve, and YieldBasis accounted for roughly 57% of Threshold’s DeFi TVL.

Aave growth shows tBTC is gaining collateral utility; Curve and YieldBasis show tBTC has deeper swap and LP infrastructure. Neither directly creates Threshold fees unless it pulls new mint or redemption flow. Static TVL supports stickiness; turnover drives revenue.

The supply KPI to watch is integration depth, DeFi TVL and utilization on major venues, rather than raw integration count. Q2’s question is whether Aave, Curve, and YieldBasis can keep absorbing tBTC after the Apr. 15 mint-fee activation, and whether that depth converts into new mint flow.

Competitor Analysis

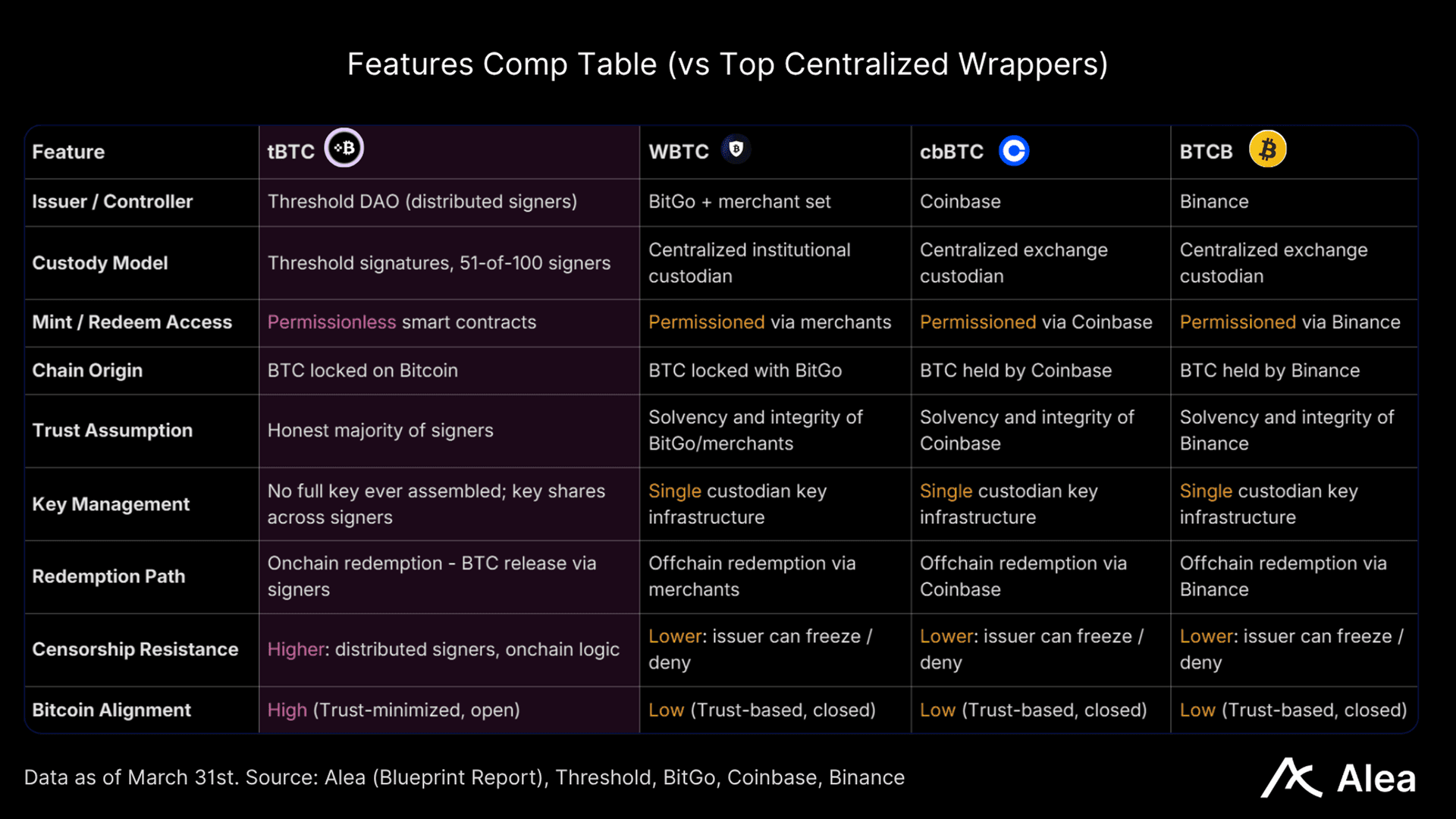

BTC wrappers compete on two axes: trust model and usable liquidity. WBTC, cbBTC, and BTCB set the liquidity ceiling, but they rely on centralized or exchange custody. tBTC, SolvBTC, ckBTC, Lombard, and uBTC compete for users who want lower single-custodian risk, but still need deep venues, borrow access, and reliable redemption.

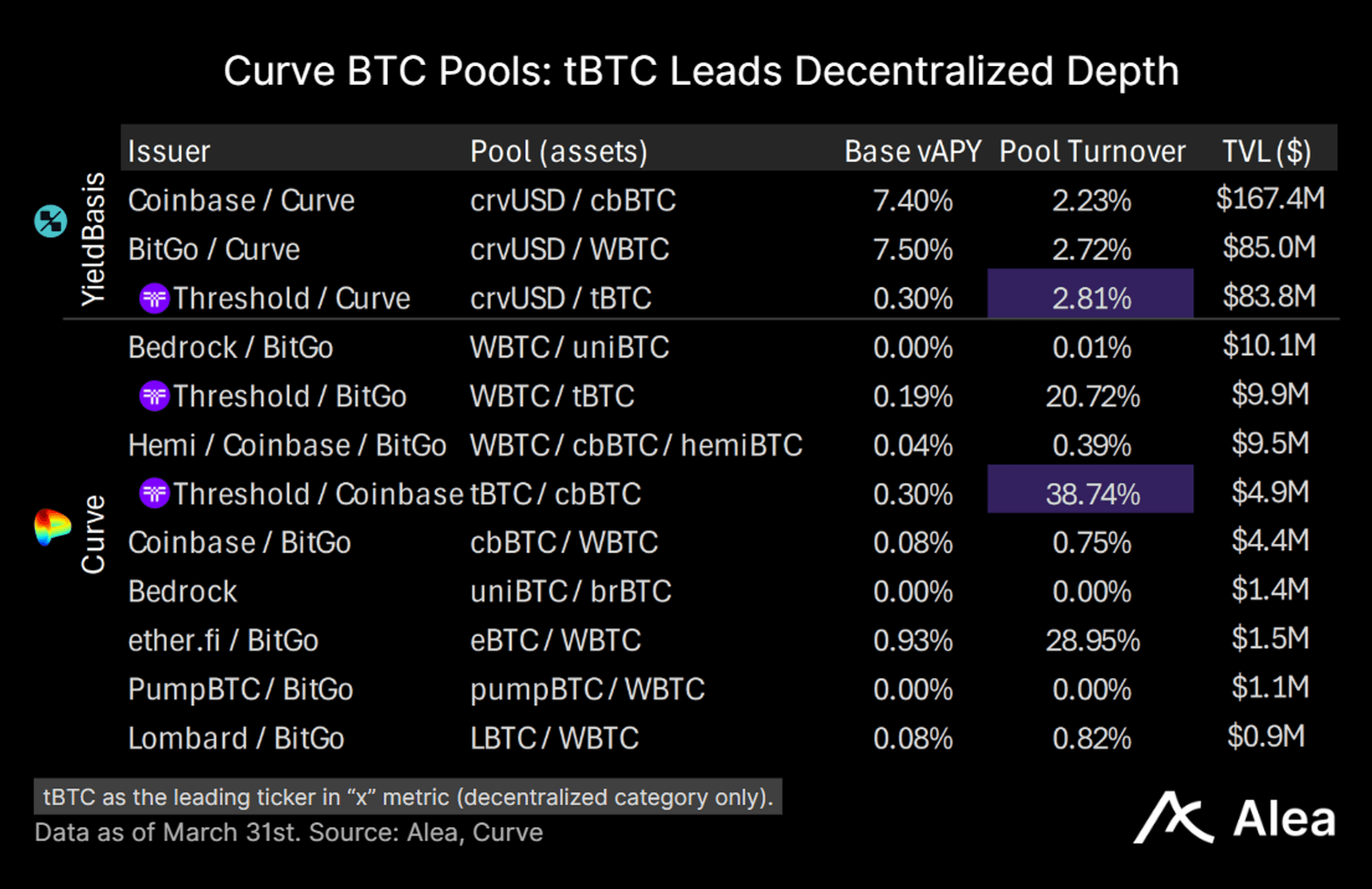

tBTC leads the decentralized wrapper set on liquidity quality (leading 6 of 8 liquidity depth metrics), with $481M of DeFi TVL and 26 integrations above $1M by the end of Q1. That makes tBTC the strongest decentralized BTC wrapper by breadth and DeFi depth.

Against centralized wrappers, however, tBTC remains subscale. WBTC and cbBTC still dominate absolute supply, daily volume, Aave scale, and top-pool depth.

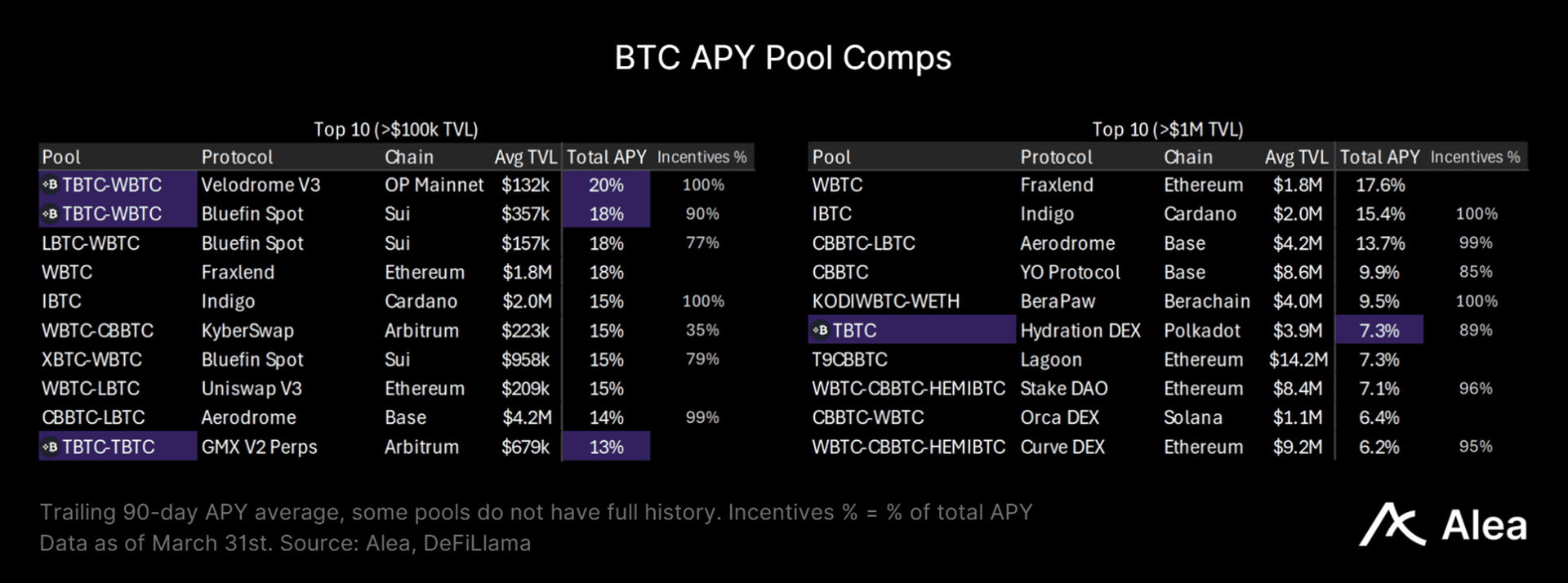

Among BTC APY pools with >$100k TVL, tBTC appears in three of the top 10 by APY, including the top two. By average TVL, Threshold’s largest APY venue is Hydration on Polkadot at 7.3% APY and ~$4M TVL.

Aave is tBTC’s clearest institutional DeFi proof point. Supplied tBTC reached ~2.1k, with borrow functionality enabled and 2.3% utilization. Utilization trails WBTC at 6.3% and cbBTC at 3.5%, but tBTC is the only decentralized BTC wrapper with borrowing enabled on Aave V3.

On YieldBasis, tBTC nearly matches WBTC in pool depth (~$84M vs $85M, a 1.4% difference, down from 4% last quarter), making it the third-largest BTC wrapper pool. This shows tBTC can compete with the largest custodial wrapper when a venue integrates it deeply.

On Curve, the tBTC/cbBTC pair again leads turnover at ~39% on ~$5M TVL, reflecting active turnover between decentralized and custodial wrappers. The WBTC/tBTC pool ($10M TVL) is the second deepest BTC-only pair on the Curve, with a $200k gap to being first (WBTC/uniBTC has 0.01% turnover vs tBTC’s ~21%).

T is one of only two issuers in this comp set with 100% float, ranking fourth by market cap. That removes unlock risk, although it does not solve token capture. The market still needs proof that tBTC’s liquidity lead converts into mint/burn fee revenue after the Apr. 15 mint-fee activation.

tBTC is not trying to beat WBTC and cbBTC on a raw scale today. It is trying to be the liquid, trust-minimized alternative that institutions can actually use. Q1 supports that claim on Aave, YieldBasis, and Curve.

What else can we read on the latest Report?

The latest Alea Research Q1 2026 Report on Threshold provides a comprehensive view that extends well beyond tBTC, covering the overall financials of the T token and the future direction of the protocol. Additional insights you can find in the report include:

- DeFi TVL Analysis for tBTC

- Fees and Protocol Revenue

- T Token Market Performance

- tBTC Market Performance

- Token Volume and Turnover

- T Token multiples

- DeFi TVL/FDV analysis

- P/F and P/S (FDV)

- Significant Updates for Threshold

- Recent Vault Launches

- The Threshold 2026 Roadmap

Access the full Q1 2026 Report by Alea Research

.png)